Corporate tax in the UAE, you say? That’s right, it’s here and it’s changing the game for Free Zone entities. Think your business isn’t affected? Well, think again. Whether you’re scratching your head over what this means, or even if you’re just plain curious, you’re in the right place.

This article will unpack everything you need to know about Free Zone Taxation in this new Corporate Tax era. From understanding who is considered a Free Zone Person to navigating different business activities and their tax implications, we’re diving deep into the maze that is taxation in a Free Zone. Read on, because trust me, this is one ride you don’t want to miss out on.

Let’s Begin….

To understand the impact of Corporate Tax on Free Zone Persons, we first need to know that in the context of UAE tax laws, persons are generally categorized into two types: Natural Persons and Juridical Persons.

1) Natural Persons:

- These include individuals who are doing business independently and in their own capacity. Examples are freelancers, sole establishments, and civil companies.

- An important point to note is that even if these persons conduct their business from a Free Zone, they cannot be recognized as Free Zone Persons under UAE tax laws.

2) Juridical Persons:

- This category comprises corporate entities such as Limited Liability Companies, among others.

- A significant distinction is that these persons can be considered as Free Zone Persons, provided they have been incorporated in a Free Zone.

These classifications play a vital role in understanding tax liabilities, especially in the context of the UAE’s Corporate Tax Law and related regulations. As we move forward, these basic definitions will help us delve deeper into the Free Zone tax concept.

With regards to the UAE Corporate Tax applicability, a Free Zone Person (FZP) can be categorized into two types.

- Qualifying Free Zone Person (QFZP): A QFZP meets certain specified conditions as set out in the tax regulations (to be explained later in this article). A QFZP can enjoy certain tax benefits (e.g. 0% tax on qualifying income), as stipulated in the legislation.

- Non-Qualifying Free Zone Person (NQFZP): An NQFZP, on the other hand, is a FZP that does not meet the specific conditions required to be a QFZP. As such, an NQFZP may not have access to the same tax benefits or exemptions as a QFZP.

Understanding the above two classifications is important, as it determines the tax liabilities and benefits applicable to an entity operating within a Free Zone.

Tax Rates for Free Zone Companies

Corporate Tax shall be imposed on a Qualifying Free Zone Person at the following rates:

- 0% on Qualifying Income.

- 9% on Taxable Income that is not Qualifying Income

Who can be a Qualifying Free Zone Person?

A Qualifying Free Zone Person is a Free Zone Person that meets ALL of the following conditions

1. Meets Adequate Substance in the UAE

- Undertake core income-generating activities in a Free Zone

- Have adequate assets to conduct such activities

- Have adequate number of qualified employees to conduct such activities

- Incur an adequate amount of operating expenses to conduct such activities

2. Derives “Qualifying Income” as specified in cabinet decision no. 55 of 2023 (This shall be explained in detailed later in this article).

3. Not Elected for 9% Tax Rate Applicability

4. Complying With Arms Length & Transfer Pricing Rules

- Complies with Arms Length Transactions (Articles 34) and Transfer Pricing (Article 55) of this Decree-Law.

5. Meet the Other Specified Conditions in Cabinet Decision no. 139 of 2023

- Non-qualifying revenue is less than a specific limit (shall discuss in detail later in this article)

- Prepares Audited Financial Statements

Types of Business Activities for Free Zone Taxability

Under the UAE tax regulations, particularly as per the Cabinet Decision 139 of 2023, business activities for Free Zone taxability can be divided into three distinct categories:

- Qualifying Activities: These are a set of 13 specific activities that are explicitly mentioned in the Cabinet Decision 139 of 2023. Free Zone Businesses conducting these activities and meeting certain conditions can be considered as engaging in Qualifying Activities and may be entitled to certain tax benefits or exemptions.

- Excluded Activities: The Cabinet Decision also outlines a list of 7 activities that are considered as Excluded Activities. Free Zone Businesses involved in these activities may not be eligible for the same tax benefits or exemptions as those engaged in Qualifying Activities.

- Other Activities: This category encompasses activities that are not specifically mentioned in either the Qualifying or Excluded Activities lists. The tax implications for these activities may vary and are determined based on their specific nature and the relevant tax regulations.

List of Qualifying Activities

- Manufacturing of goods or materials.

- Processing of goods or materials.

- Holding of shares and other securities.

- Ownership, management and operation of Ships.

- Reinsurance services

- Fund management services

- Wealth and investment management services

- Headquarter services to Related Parties.

- Treasury and financing services to Related Parties.

- Financing and leasing of Aircraft, including engines and rotable components.

- ** Distribution of goods or materials in or from a Designated Zone to a customer that resells such goods or materials, or parts thereof or processes or alters such goods or materials or parts thereof for the purposes of sale or resale. (** the activity of distributing goods or materials must be undertaken in or from a Designated Zone and the goods or materials entering the State must be imported through the Designated Zone.)

- Logistics services.

- Any activities that are ancillary to the above

List of Excluded Activities

- Any transactions with natural persons, except

- Ownership & management of ships,

- Fund management services

- Wealth management Services

- Financing & leasing of aircrafts

2. Banking activities

3. Insurance activities except re-insurance activities

4. Finance and leasing activities except

- Treasury and financing services to Related Parties.

- Financing and leasing of Aircraft

5. Ownership or exploitation of immovable property EXCEPT

- Commercial Property located in a Free Zone where the transaction in respect of such Commercial Property is conducted with other Free Zone Persons.

6. Ownership or exploitation of intellectual property assets.

7. Any activities that are ancillary to the above

What is Included in Qualifying Income?

The concept of Qualifying Income in the context of UAE Free Zone tax regulations is a vital one. Qualifying Income is categorized based on the nature of the transactions and parties involved.

- Transactions with Other Free Zone Persons: Here, Qualifying Income comprises income from all transactions except those derived from Excluded Activities. This means that as long as the activity is not excluded, the income from such transactions with other Free Zone entities is considered as Qualifying Income.

- Transactions with Non-Free Zone Persons: In this case, Qualifying Income includes income from Qualifying Activities only. If the transaction involves any Excluded Activities, then the income generated from such activities will not be considered as Qualifying Income.

- Income From All Other Transactions: This includes any other income that a Qualifying Free Zone Person might earn, provided that they satisfy the de minimis requirements. These requirements usually pertain to thresholds or limits under which the income may still be considered as Qualifying Income. I will shortly explain how the de minimis requirements are calculated.

Note that Qualifying Income does not include income derived from a Domestic or Foreign Permanent Establishment (e.g. branch of a free zone company in Mainland or outside the UAE), income derived from immovable commercial property when dealing with Non-Free Zone Persons, or income from non-commercial property when dealing with either Free Zone Persons or Non-Free Zone Persons.

Tax on Income Attributable to a Domestic Permanent Establishment or a Foreign Permanent Establishment

The taxation rate for income attributable to either a Domestic Permanent Establishment or a Foreign Permanent Establishment of a Free Zone Persons is set at 9% under UAE tax regulations.

- Domestic Permanent Establishment: This term refers to a fixed place of business located within the UAE but outside a Free Zone (e.g. Mainland), through which the business of an entity is wholly or partly conducted. If income is generated through this establishment, it will be subjected to a tax rate of 9%.

- Foreign Permanent Establishment: This pertains to a fixed business operation situated outside the UAE. Income attributable to such a foreign entity will also be taxed at 9%.

Income Attributable to Immovable Property Located in a Free Zone

Income derived from immovable property located in a Free Zone in the UAE is categorized based on the type of property and the person with whom the dealings are conducted. The tax implications vary accordingly.

- Income from Commercial Property: This is immovable property used exclusively for a business or business activity and not used as a place of residence or accommodation. This category is further divided into:

1.1. Dealing with Non-Free Zone Persons: If the income is generated from transactions with non-free zone persons, it is taxed at a rate of 9%.

1.2. Dealing with Free Zone Persons: If the income is generated from transactions with other free zone persons, it is considered as Qualifying Income and taxed at a rate of 0%.

2. Income from Non-Commercial Property: This category includes income generated from immovable property not used for business purposes. Regardless of whether the dealing is with a Free Zone Person or a Non-Free Zone Person, the income is taxed at a rate of 9%

De Minimis Rule to Meet Qualifying Free Zone Person’s Condition

The de minimis rule in UAE tax law pertains to the conditions a Qualifying Free Zone Person (FZP) needs to meet regarding their Non-Qualifying Revenue. The rule stipulates that a Qualifying FZP’s Non-Qualifying Revenue should be less than the lower of 5% of their Total Revenue or AED 5 million (whichever is less).

Non-Qualifying Revenue: This refers to revenue derived in a tax period from the following sources:

- Excluded Activities

- Activities that are not Qualifying Activities where the other party to the transaction is a Non-Free Zone Person.

Total Revenue: This includes all revenue derived by a Qualifying Free Zone Person in a tax period.

Exclusions from Non-Qualifying & Total Revenue

Certain types of revenue are excluded from both Non-Qualifying and Total Revenue calculations. These exclusions include:

- Revenue attributable to immovable property located in a Free Zone from the following transactions: – Transactions with Non-Free Zone Persons in respect of Commercial Property – Transactions with any person in respect of immovable property that is not Commercial Property

- Revenue attributable to a Domestic Permanent Establishment or a Foreign Permanent Establishment of the Qualifying Free Zone Person.

To summarize:

The de minimis rule for Qualifying Free Zone Persons states that their Non-Qualifying Revenue, which includes income from Excluded Activities and activities not considered as Qualifying when dealing with Non-Free Zone Persons, must be less than either 5% of their Total Revenue or AED 5 million. The Total Revenue comprises all income generated by the Qualifying FZP in a given tax period. Certain revenue types, notably those connected to immovable property within a Free Zone and revenue tied to a Domestic or Foreign Permanent Establishment, are excluded from these calculations.

Example – De Minimis Rule

Let’s consider an example for the de minimis rule to make it easier to understand.

Suppose there is a business called ‘XYZ Tech LLC’ in a UAE Free Zone which has two types of revenues:

- Qualifying Revenue (from Qualifying Activities with other Free Zone Persons and Non-Free Zone Persons): AED 80 million.

- Non-Qualifying Revenue (from Excluded Activities and activities with Non-Free Zone Persons that are not Qualifying Activities): AED 6 million.

Let’s apply the de minimis rule:

First, calculate 5% of the total revenue: 5% of AED 86 million = AED 4.30 million.

The de minimis rule states that Non-Qualifying Revenue should be less than the lower of 5% of total revenue or AED 5 million (whichever is lower). In this case, 5% of total revenue (AED 4.30 million) is less than AED 5 million, hence our benchmark to compare will be AED 4.30 million.

But, XYZ Tech LLC’s Non-Qualifying Revenue is AED 6 million, which is greater than AED 4 million. Therefore, XYZ Tech LLC does not meet the de minimis rule because its Non-Qualifying Revenue exceeds the threshold set by the rule. As a result, the company would not be considered a Qualifying Free Zone Person for tax purposes.

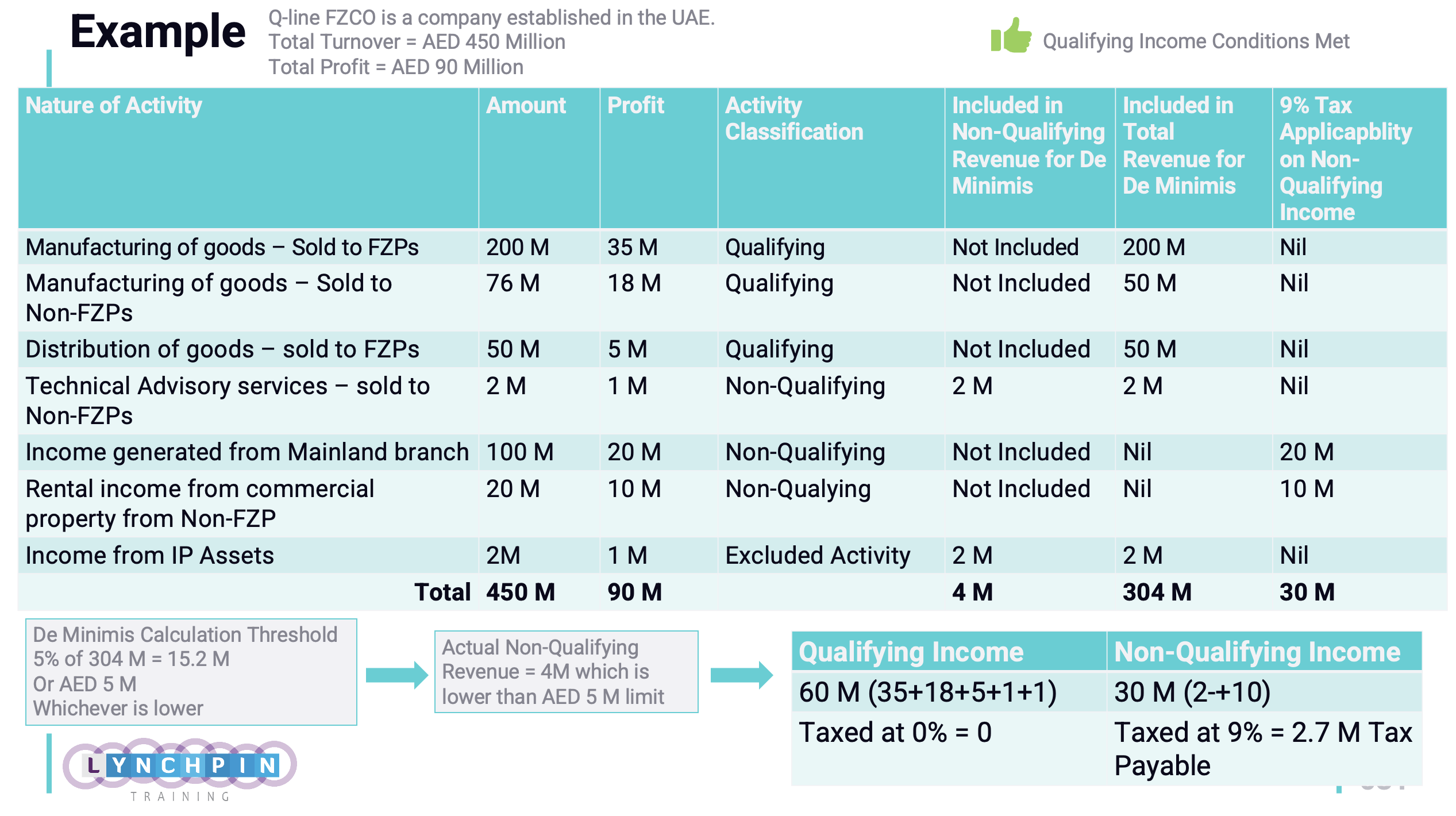

Example: Corporate Tax Calculation for a Qualified Free Zone Person

Having covered the vital concepts surrounding Free Zone Tax implications, let’s now delve into a comprehensive illustration. This example elucidates how the Corporate Tax calculation unfolds for a Qualifying Free Zone Person.

Conclusion & Next Steps

In conclusion, the new UAE Corporate Tax regime provides a competitive and favourable environment for companies incorporated in Free Zones. Understanding the tax implications and structuring business transactions and operations accordingly is crucial to optimising the benefits of being a Free Zone entity.

Companies should pay attention to the nature of their activities (qualifying vs. excluded), their customer base (Free Zone Person vs. Non-Free Zone Person), and the types of assets they own (Commercial Property vs. Non-Commercial Property). Even though a Free Zone entity might have certain non-qualifying revenues, the de minimis rule could allow the entity to still be considered a Qualifying Free Zone Person if certain conditions are met.

I hope this guide gives you a better understanding of the Free Zone Taxation concept under the UAE’s new Corporate Tax regime. As always, tax matters are complex and often require a tailored approach for each business. That’s where our experienced team can help.

For more information or consultation on Corporate Tax and other related services, feel free to reach us here, or call us directly at +971-58-5915700. We’re more than happy to guide you through this process and help your business thrive under the new tax regime.